There’s something quietly unsettling about watching a stranger walk through your home with a clipboard, a camera, and the power to influence hundreds of thousands of dollars of your financial future. Home appraisers are trained observers. They’re not just looking at square footage or how fresh the paint looks. They’re reading signals, and those signals tell a surprisingly detailed story about how you manage, prioritize, and protect your most valuable asset.

Most homeowners focus on staging for buyers or cleaning up for guests. An appraiser, though, is a different kind of visitor entirely. A home appraisal is an unbiased, professional assessment of your property’s current market value conducted by a licensed appraiser. What they see the moment they step through your door reveals far more about your financial decision-making than you’d expect. Let’s dive in.

1. The Condition of Your Roof Signals Whether You Play Financial Defense

Here’s the thing about roofs – nobody thinks about them until water is dripping into the living room. A well-maintained roof tells an appraiser that you’ve been proactive, not reactive, with your spending. Appraisers look for a roof that keeps moisture from entering the home, and a roof that needs to be replaced within two years must be reported.

That single notation on an appraisal report can cascade into a lower valuation, renegotiated contracts, or even a failed loan. Property condition issues beyond normal wear and tear can significantly impact value, and major deferred maintenance, structural problems, or safety hazards typically result in lower appraisals. Ignoring a roof isn’t just a maintenance issue – it’s a financial statement.

2. Your Curb Appeal Tells Them What You Value First

An appraiser forms a first impression before they even ring the doorbell. Overgrown bushes, a cracked driveway, peeling exterior paint – these aren’t just aesthetic problems. They’re clues about where you direct your money and attention. Piles of building materials or a rusting appliance outside can raise questions about whether there are foundation or soil issues.

Think of curb appeal like a handshake. It’s not the whole person, but it frames everything that follows. You don’t have to spend thousands renovating – it’s about addressing the little things that can distract an appraiser and start to add up when they compare your home to others in the neighborhood for the final valuation. A tidy exterior says you’re on top of things. A neglected one says you might not be.

3. Deferred Interior Maintenance Speaks Volumes

Walk into most homes and you’ll spot the signs quickly – a hole in the drywall never patched, a door that doesn’t close properly, a dripping faucet that’s been dripping for two years. These are what appraisers call deferred maintenance, and they’re financial red flags wrapped in inconvenience. Damage like a hole in the drywall or a missing board on a porch can distract from an otherwise good-condition property or cause the appraiser to make deductions for “unknown condition.”

Deferred maintenance is essentially borrowing against your future home value. Low appraisals can result from poor property condition, outdated features, lack of comparable sales, market volatility, or inflated listing prices that don’t align with recent sales data. It’s not dramatic – it’s death by a thousand small financial cuts. An appraiser sees all of them at once.

4. Kitchen Upgrades (or the Lack of Them) Reveal Your Investment Mindset

Kitchens are where financial priorities become almost painfully obvious. A homeowner who has invested in quality countertops, working appliances, and sensible cabinetry is signaling long-term thinking. One who has let a twenty-year-old kitchen sit untouched while spending money elsewhere is signaling something very different. Appraisers look at kitchen appliances, materials used throughout the home, and the overall condition of both exterior and interior elements.

I think of the kitchen as the financial heartbeat of a home. It’s the room most buyers scrutinize and most appraisers weight heavily in their comparisons. The appraiser researches recently sold properties in your area with features similar to your prospective home, called comparables, and appraisers and real estate agents use at least three of these, usually through the Multiple Listings Service, to get the most accurate estimate possible of a home’s value. If your kitchen underperforms those comps, the number drops.

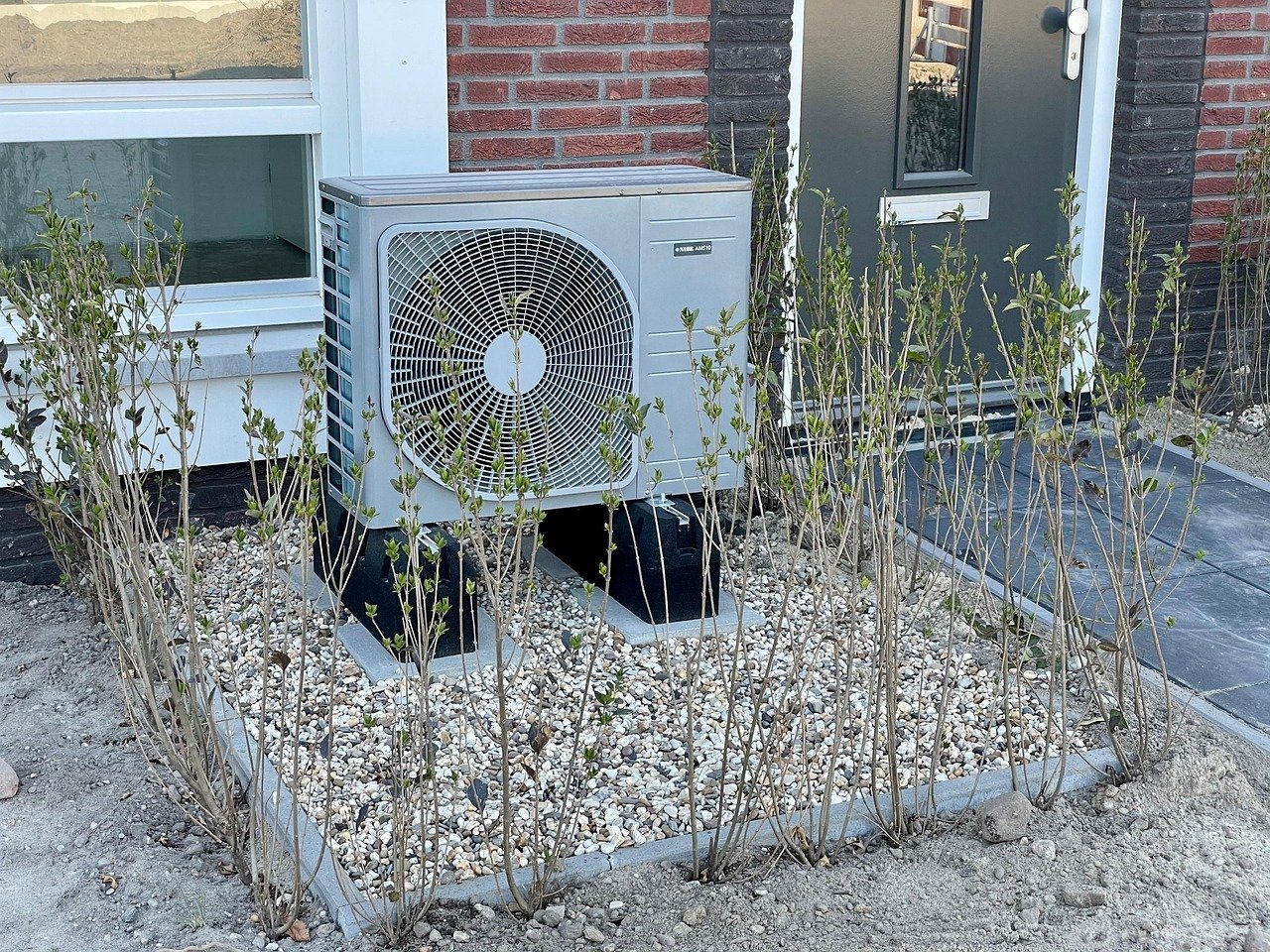

5. The State of Your HVAC System Shows Whether You Think Long-Term

An HVAC system is one of the least glamorous things you can spend money on. It’s invisible, unglamorous, and wildly expensive when it fails. That’s exactly why appraisers pay attention to it. A well-serviced heating and cooling system tells the story of a homeowner who budgets for the unsexy but critical stuff. Appraisers examine the HVAC system as part of their evaluation of walls, floors, carpeting, kitchen appliances, bathrooms, and overall materials throughout the home.

A failing or outdated HVAC system can signal financial avoidance – the pattern of postponing costly but necessary repairs until they become unavoidable emergencies. Appraisers note obvious defects that might affect value, even though they aren’t searching for hidden problems or conducting detailed systems testing. If the system looks ancient or poorly maintained, it shows up in the valuation. Every time.

6. The Bathroom Condition Tells a Story About Incremental Investment

Nobody expects a bathroom to look like a luxury hotel. But appraisers notice when a bathroom has been maintained versus quietly neglected. Cracked grout, leaky fixtures, outdated ventilation, and peeling caulk are all signals that incremental, affordable upkeep hasn’t happened. Appraisers look at bathrooms and are generally looking for items that are a safety hazard, broken, or malfunctioning in both exterior and interior elements.

The financial insight here is subtle but real. Bathrooms are one of the cheapest rooms to maintain yet carry heavy weight in appraisals. Spending a few hundred dollars a year on small bathroom repairs is a smarter financial move than the thousands in deductions that result from complete neglect. Minor repairs like dripping faucets should be addressed if at all possible before an appraisal visit. Small habits, big implications.

7. Documented Renovations Show You Understand Return on Investment

Here’s something many homeowners genuinely don’t know: the presence of documentation for improvements is itself a sign of financial sophistication. Receipts for a new roof, permits for an addition, work orders for a kitchen remodel – these all tell an appraiser that you’ve been investing strategically, not randomly. The appraisal process goes more smoothly and is more accurate if you can provide documentation of any work you’ve done on the property, including receipts for repairs, inspection reports, work orders for major renovations, and receipts for materials used.

Undocumented improvements, on the other hand, create uncertainty. An appraiser who cannot verify that work was done properly, or with proper materials, has to hedge. These documented details are helpful data points for the appraiser when creating adjustments against comparable sales in the area. No paper trail means a conservative estimate. It’s that simple.

8. Foundation and Structural Integrity Reveal Your Risk Tolerance

Nothing cuts through financial conversation quite like foundation issues. Whether hairline cracks in a basement wall or moisture in a crawlspace, structural concerns broadcast one thing clearly: this homeowner accepted significant financial risk by leaving this unaddressed. The foundation should be stable and free of cracks or other damage, and the crawlspace, if present, should be well-ventilated and free of moisture or pests.

Honestly, structural deficiencies are the appraisal equivalent of maxing out your credit card and hoping nobody notices. The deal-breaker issues tend to be serious problems that cannot easily be corrected. Appraisers aren’t there to judge your lifestyle, but when structural red flags appear, they directly threaten the home’s lendability, its value, and ultimately your equity position.

9. Energy Efficiency Features Signal Forward-Thinking Financial Planning

In 2025 and beyond, energy efficiency isn’t just a feel-good upgrade. It’s a measurable contributor to appraised value. Insulation quality, double-pane windows, modern water heaters, and smart thermostats all tell an appraiser that the homeowner thinks beyond the monthly mortgage payment. Documentation of materials like insulation demonstrates that a homeowner has used the right products, which serves as supporting evidence during the appraisal.

Homes with documented energy efficiency improvements are increasingly relevant in today’s market, where inflation remains persistent, with shelter costs rising notably and buyers are more cost-conscious than ever. Lower utility costs increase a home’s attractiveness to buyers, which influences comparable sales and, in turn, appraisal outcomes. That’s not theory – that’s how the math works.

10. Clutter and Access Issues Signal Financial Disorganization

This one might sound unfair, but stay with me. Excessive clutter doesn’t get counted against you on an appraisal form in the same way a cracked foundation does. What it does, though, is prevent the appraiser from properly accessing and evaluating the property. And that creates problems. Appraisers need to access all areas of the home, which means clutter from doorways and halls must be cleared, room doors must open and close freely, and basement steps must be free of tripping hazards.

When access is restricted, appraisers are forced to note conditions as “unknown,” which leads to conservative estimates. Think of it this way: if you show up to a job interview in a wrinkled shirt, it doesn’t mean you’re bad at the job – but it does shape the perception. A home appraisal is an unbiased professional opinion of a property’s fair market value, and the appraiser’s job is to provide an objective assessment of what a property is actually worth in the current market. Anything that clouds that objectivity works against you.

11. The Overall Maintenance Pattern Shows Whether You Treat Your Home as an Asset

When an appraiser steps back and takes in the full picture, they’re doing something almost instinctive: they’re assessing whether this homeowner views their property as a true financial asset or just a place to live. There’s a big difference, and it shows. Appraisers conduct a systematic evaluation both inside and outside your home, taking photographs of each room, detailed notes, and measurements.

The overall pattern of maintenance is the most telling signal of all. Appraisers assess the property’s size, layout, condition, recent upgrades, location, and neighborhood factors, and they also analyze recent comparable sales to support their valuation. A home where everything works, nothing is deferred, and improvements are documented tells a story of financial discipline and strategic ownership. That story has real dollar value attached to it.

In the current market, where the average cost of a single-family home appraisal sits around $357 according to 2025 data, and where roughly one in twelve pending home sales appraised below the contract price in mid-2024 according to CoreLogic, the stakes have never been more real. Every choice you make about maintaining, upgrading, or documenting your home is a financial decision – and appraisers read every single one of them the moment they walk through your door.

What surprises you most about what an appraiser picks up on? Tell us in the comments.