You probably don’t think much about the 90 seconds you spend at the teller window. Hand over the check, sign the slip, grab your receipt, done. Simple, routine, forgettable. Except it isn’t – not from the other side of that counter.

Bank tellers are trained observers. They’re not just processing paper; they’re reading a surprisingly detailed story about your financial life in the time it takes you to look up from your phone. Some of what they notice is procedural, some of it is legally required, and some of it is just pattern recognition built from thousands of daily interactions. Let’s dive in.

1. Whether Your Account Balance Can Actually Cover the Check

![1. Whether Your Account Balance Can Actually Cover the Check (CarbonNYC [in SF!], Flickr, CC BY 2.0)](https://happywallet.co/wp-content/uploads/2026/03/1773885710471_1773885706541_2204277278_cbf43f4146_b.jpeg)

This is the very first thing a teller checks, and it happens in seconds. Bank tellers can see the amount of cash you have stashed in your bank account, including other personal information. The moment your profile pops up on their screen, your balance is right there, no mystery about it.

In addition to checking your balance, bank tellers may also check to know your account’s status and whether it is in good standing with the financial institution. If you’re regularly pushing your balance to the edge, that pattern is visible too. It’s not judged out loud, but it’s noticed.

Here’s the thing – a low balance on the day you’re depositing a large check creates its own kind of flag. Possible examples of transactions that might prompt questions from a teller include large dollar deposits to typically lower balance accounts. Think of it like showing up with a suitcase full of luggage when you’ve never owned more than a backpack.

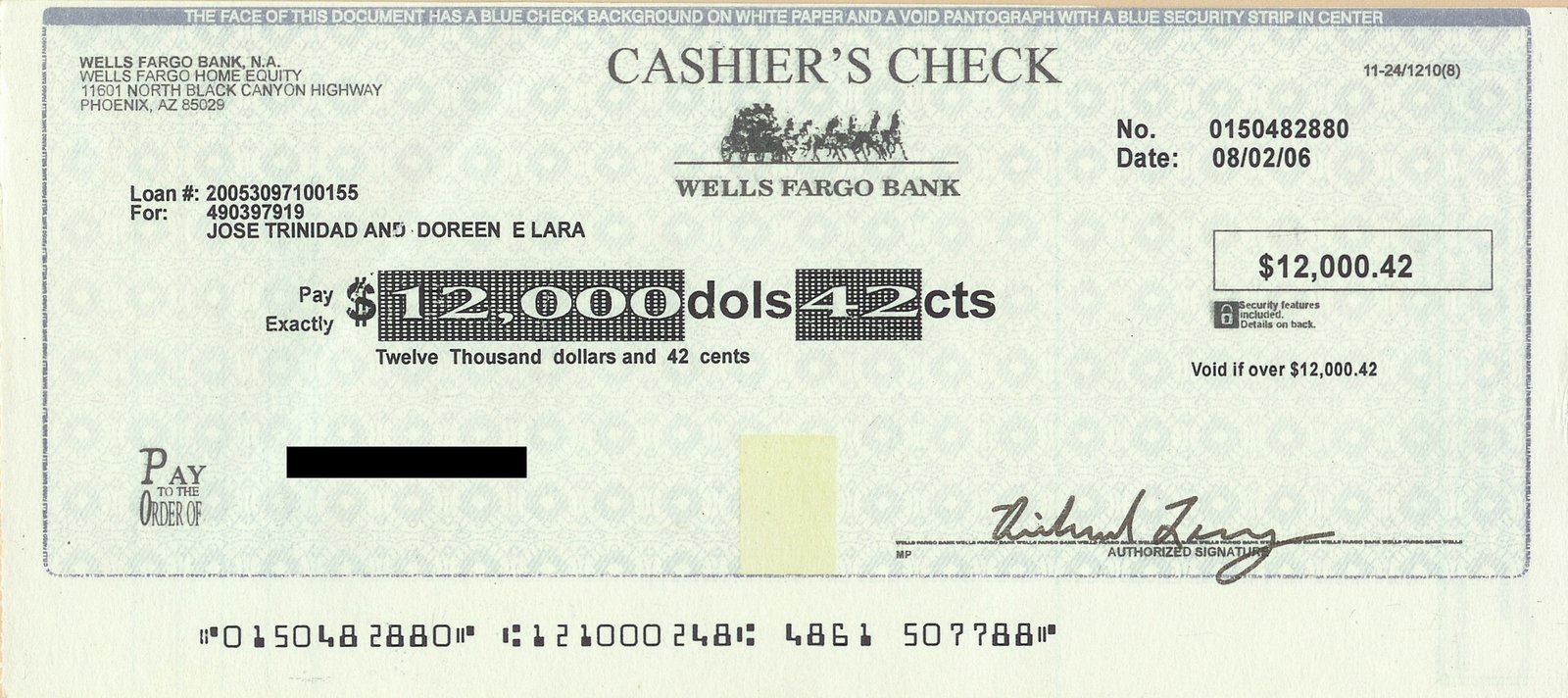

2. Red Flags in the Check’s Physical Appearance

Tellers are essentially the last human line of defense against check fraud, and they know it. They’re trained to look at a check physically before they touch a single key. FinCEN’s September 2024 Financial Trend Analysis reports that counterfeit checks are often made using incorrect check stock and security features – features that may be detected through an in-person deposit.

Tellers are taught to recognize signs like altered ink, inconsistent handwriting, or multiple checks from unrelated accounts. A check that looks slightly “off” – smudged print, faded watermarks, paper that doesn’t feel right – is enough to trigger a pause. Most customers never even realize the scrutiny is happening.

The stakes here are enormous. In 2023 and 2024, check fraud accounted for a significant portion of payment fraud losses, with financial institutions losing over $1.3 billion in the United States alone. That context is why tellers are thorough, not paranoid. They’re protecting you as much as the bank.

3. Whether Your Signature Matches What’s on File

Honestly, this one surprises a lot of people. Bank tellers validate signatures. So, aside from the balance, they’ll check to know if your signature matches the one on the withdrawal slip, etc. That signature card you filled out when you first opened your account? It still matters every single time.

According to a FinCEN mail-theft trend analysis report from September 2024, check altering is the most frequently used method of check fraud, accounting for approximately 44% of Bank Secrecy Act (BSA) reports. Signature discrepancies are often where altered checks get caught. It’s a simple but powerful check that has existed since banking began.

Fraudulent signature was the third most frequent method of check fraud used, accounting for 20% of BSA reports according to FinCEN. So when a teller tilts their head and studies your signature a beat longer than usual, know that they’re doing exactly what they’re supposed to do.

4. Whether the Transaction Amount Crosses the $10,000 Reporting Threshold

There is a very specific line that changes everything once you cross it. The Bank Secrecy Act has required financial institutions to report any cash transactions exceeding $10,000 within a single business day by filing a Currency Transaction Report (CTR) for over 50 years. That report goes directly to federal authorities.

When a transaction involving more than $10,000 in cash is processed, most banks have a system that automatically creates a CTR electronically, and tax and other information about the customer is usually pre-filled by the bank software. The teller doesn’t necessarily have to do much manually – the system flags it for them. But they are absolutely aware it’s happening.

What’s worth knowing is the context around that threshold. The $10,000 threshold was established in 1972 upon enactment of the Bank Secrecy Act and would exceed $75,000 if adjusted for inflation as of February 2024. In other words, the bar has stayed frozen while the economy has grown dramatically around it. More transactions hit that wire than ever before.

5. Signs of “Structuring” – Deliberately Staying Under the Threshold

Here’s something most people don’t realize: trying to avoid that $10,000 reporting requirement by making smaller deposits is itself a federal crime. It’s called structuring, and bank tellers are specifically trained to spot it. The Bank Secrecy Act requires financial institutions to file reports if the daily aggregate exceeds $10,000, and to report suspicious activity that may signify money laundering, tax evasion, or other criminal activities.

CTRs since 1996 include an optional checkbox at the top if the bank employee believes the transaction to be suspicious or fraudulent, commonly called a Suspicious Activity Report (SAR). If a teller suspects structuring, they can file a SAR even if each individual deposit is technically under the threshold. The pattern matters as much as the number.

Multiple trips in the same day, unusual urgency, or deposits that feel like they’re “just below” a round number – all of these can raise a quiet alarm. It’s not accusatory, but tellers are paid attention to these rhythms. Financial institutions are required to verify a customer’s identity and retain records of certain information prior to issuing monetary instruments when purchased with currency in amounts between $3,000 and $10,000.

6. How Often You Visit – and Whether Your Pattern Has Changed

Regulars are recognizable, and so are their habits. A customer who comes in every Friday to deposit a paycheck has a very readable financial rhythm. When that rhythm suddenly changes – larger deposits, different times, new payees – tellers notice. Banks train staff to identify checks written for large amounts that deviate from a customer’s usual behavior, and unusual recipients of checks from a known customer.

A bank teller that knows your financial struggles or dealings over the years won’t hesitate to raise the alarm when you approach the bank to transfer money to a country you have never done business in. That long-term pattern recognition is part of their job, even if it rarely comes up in casual conversation.

Think of it like a neighborhood barista who notices when a regular suddenly orders a double espresso instead of their usual decaf. It probably means nothing. Still, it registers. At a bank, that registration carries legal weight.

7. The Age and Validity of the Check Itself

If you have ever found an old check in a forgotten jacket pocket and tried to cash it months later, you already know this can be a problem. You go to deposit it, only to find out that the check has expired. Depositing checks promptly can help you avoid potential issues with check expiration or stale dating.

Most personal checks are considered valid for 180 days after the date written. Business checks can have even shorter windows. Tellers check the date automatically – it’s one of the first things they scan. A stale check doesn’t just get flagged; it often gets outright refused, which can create genuine financial headaches if you weren’t expecting it.

The broader trend here is worth noting. The Federal Reserve reports that while paper check usage continues to decline, the average value per check has risen, reaching approximately $2,738 in 2024, up from $2,692 in 2023. Higher value checks with expired dates represent a compounding problem that tellers deal with regularly.

8. Whether the Check Comes From a Known Fraud-Prone Source

Not all checks are treated equally at the window, and the source matters. Tellers have access to internal and industry-wide fraud databases. Many banks are pushing their tellers to get accounts to access free-to-members ABA Frontline Compliance Training, which includes courses on check fraud. ABA also offers a check fraud toolkit and the ABA Fraud Contact Directory, which includes inside contact info for fraud claims for half of all banks in the U.S.

Teller line validation of on-us checks – a check that is deposited or cashed at the same financial institution from where it was written – plays a critical role in catching fraudulent checks presented to be cashed at the branch. That means your teller is actively cross-referencing details, not just glancing at the paper in their hand.

Bad actors are preferring deposit methods that avoid in-person contact – opening their depository accounts online and using ATMs or mobile and remote deposits. Ironically, the teller window has become one of the safer places in banking precisely because a human being is standing there paying attention.

9. Incomplete or Incorrect Information on Your Deposit Slip

This one is less dramatic but far more common than you might expect. Incomplete or inaccurate deposit slips are so common. Customers often forget to sign the slip or enter the correct account number. This happens so frequently that many banks will ask you to use your ATM card and PIN at the teller line so they can view your correct accounts on their screen and double check.

The consequence of a wrong account number isn’t small. The main problem with this mistake is risking having your cash deposited into the wrong account, and getting it back out can be a hassle and a challenge. Tellers catch this constantly, and they quietly correct it without making a scene – though they do take note of the error.

There’s a broader picture here too. The most common mistake banking customers make on a daily basis is not keeping track of their deposits – and they should be. Sloppy paperwork is a window into how organized a customer is with their money overall. It’s not something tellers report, but it shapes the interaction from that point forward.

10. Your Overall Account Health and Financial Standing

The moment your profile loads, a teller can see far more than just a balance. They can see your account history, whether you have overdrafts on record, and whether there are holds or restrictions on your account. Account information such as product ownership, account balances, and tenure with the bank, combined with transaction data including frequency, volume, and types of transactions, is all visible in a customer profile.

Financial stress is a reality for most Americans. In fact, only about fifteen percent of people say they’re not experiencing any of the common financial stressors. Tellers see that stress reflected in account patterns every single day – repeated overdrafts, minimal savings balances, and paycheck-to-paycheck timing.

What’s striking is that this information can work in your favor too. A teller who sees you’ve maintained a long, healthy account history is more likely to extend professional courtesies – like expediting a hold release on a deposited check. Your account health is essentially your financial reputation at that branch, and it walks in the door before you say a word. Retail bank customers interact with their bank every three days, on average, across a combination of digital, phone, and in-branch channels, and the tenor of those interactions has a massive influence on customer satisfaction and overall levels of trust.

Conclusion

That brief moment at the teller window is more layered than most people ever suspect. A trained human eye, a loaded software dashboard, and years of pattern recognition all converge in the few seconds it takes to hand over a piece of paper. It’s not surveillance – it’s the system working as it’s designed to.

The good news is that for the vast majority of customers, none of this matters in any alarming way. Keep your account in reasonable shape, deposit checks promptly, fill out your slip carefully, and the interaction stays exactly what it should be: quick, professional, and completely unremarkable. The more you know about what’s happening behind that glass, the more confidently you can walk up to the window.

What surprised you most about what tellers can see? Tell us in the comments.