Avoiding these common pitfalls is essential to maximize success with Dave Ramsey’s plan.

Dave Ramsey’s financial plan offers a clear roadmap for managing money and eliminating debt, but several common mistakes can derail progress. Many people struggle by skipping budget creation, ignoring emergency funds, or taking on new debt while paying off old loans. Understanding and sidestepping these errors ensures a smoother journey toward financial stability and achieving long-term goals with confidence and control.

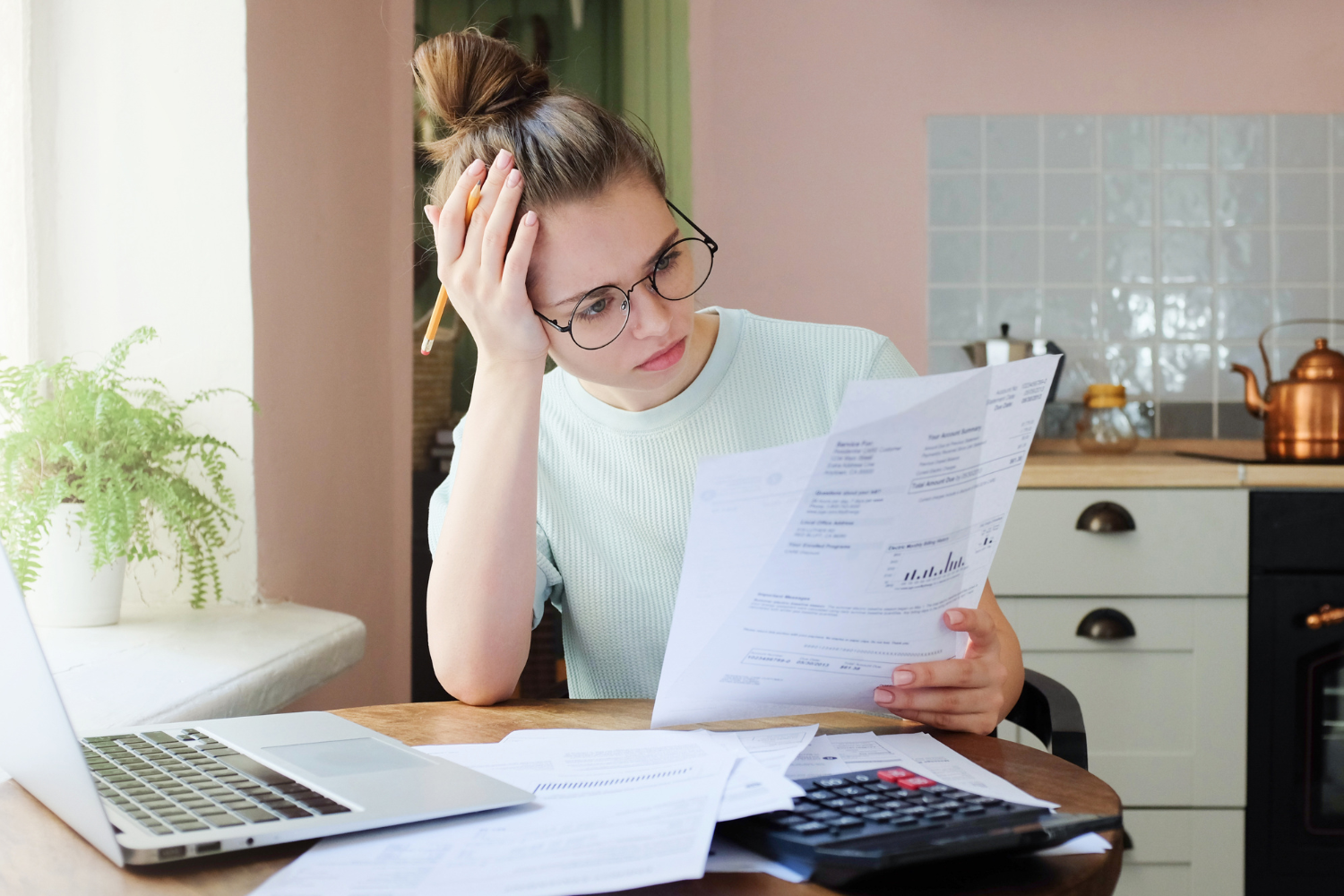

1. Overlooking the importance of a detailed monthly budget.

Creating a detailed monthly budget serves as the cornerstone of personal finance. Everyone experiences fluctuating expenses, like a sudden car repair or medical bill. By laying out expected costs and setting limits, the budget clarifies spending decisions, reducing surprise outlays during the month.

Without this financial map, overspending becomes likely, leaving little room for saving. When the budget is meticulously planned, like mapping out a cross-country road trip, it ensures funds are allocated appropriately, allowing goals to be achieved systematically.

2. Ignoring the need to build a starter emergency fund early.

Building a starter emergency fund establishes a safety net for unexpected financial shocks. Often an afterthought, this fund acts like a financial buffer, covering sudden expenses without derailing long-term goals. Starting small, even if it’s the cost of a family meal, sets a crucial foundation.

Neglecting this initial step can lead to increased debt during financial emergencies. Creating this reserve early on provides peace of mind, ensuring that unplanned costs don’t require dipping into savings meant for other objectives.

3. Relying on credit cards instead of prioritizing debt payoff.

Credit cards can provide convenience, yet they frequently lead to more debt, opposing the goal of financial freedom. A swipe feels light, but the interest builds weightily over time. Prioritizing debt elimination rather than accruing more aligns with successful financial management.

Emphasizing debt payoff over charging new expenses prevents the cycle from repeating. The sense of relying on cash shifts mindset and empowers incremental victories in debt reduction rather than adding to financial burdens.

4. Skipping the step of saving for unexpected expenses.

Saving for unexpected expenses is a preventative measure that often gets skipped. Just like forgetting an umbrella, ignoring this step leaves one vulnerable when unforeseen costs arise. By planning for these surprises, financial stability is maintained even when skies turn gray.

Failure to allocate funds for these expenses can derail financial progress. Consistently setting aside even small amounts builds a reserve that mitigates immediate trauma, allowing other financial goals to stay intact.

5. Neglecting to fully understand the baby steps in order.

Understanding the baby steps in proper sequence is vital for consistent progress. The methodology is structured for gradual success, addressing immediate needs before long-term aspirations. Skipping or rearranging steps can result in a shaky foundation, much like constructing a house without a blueprint.

Lack of clarity in these steps often leads to confusion and inefficiency. Knowing the exact order prevents common pitfalls and ensures every move aligns with future objectives, leading to sturdy financial architectures.

6. Underestimating the impact of lifestyle inflation on budgeting.

Lifestyle inflation quietly pressures budgets, often underestimated until unchecked habits surface. As income rises, desires expand, and spending often balloons without reflection. The danger lies in growing accustomed to these new standards, making financial control challenging without mindful monitoring.

Recognizing this inflation helps adjust and stabilize finances. By identifying and countering shifting spending patterns, one maintains control, much like a pilot course-correcting through turbulent skies to ensure financial journey resilience.

7. Failing to communicate openly about money with family members.

Communication about money with family members shapes shared financial outcomes. Each person’s goals and contributions affect the entire household’s financial landscape, much like different instruments in an orchestra. When these conversations don’t happen, misunderstandings and conflicts arise.

Clear dialogue fosters alignment, avoiding overspending or clashing decisions. The transparency creates a unified approach, paving a smoother financial path enjoyable for all contributors, each playing their part harmoniously.

8. Avoiding tracking spending habits and financial progress regularly.

Avoiding regular expense tracking leaves spending unchecked and savings elusive. Reviewing habits illuminates patterns that might otherwise go unnoticed, like the small leaks that sink ships. When tracking becomes routine, achieving goals feels more tangible, like assembling a complex puzzle piece by piece.

The consistency provides a snapshot of financial health, allowing adjustments before issues spiral. Knowing exactly where money flows curtails unnecessary outflows and reinforces discipline, painting a clearer path to financial well-being.

9. Taking on new debt while still paying off previous loans.

Taking on new debt while paying off old loans endlessly extends the repayment cycle. Each new obligation, regardless of size, reinforces the mountain of financial commitment. Bridging debt has the unsettling result of never-ending payments and financial stagnation.

Refraining from acquiring additional debt maintains focus on existing repayment. Avoiding new debt means taking deliberate steps to lower financial burdens, ultimately leading to a sense of empowerment through intentional fiscal discipline.

10. Overcommitting financially without a clear savings and repayment plan.

Committing financially without clear plans increases vulnerability to missteps. When impulsive decisions override structured saving and repayment plans, the results are unpredictable, like jumping into water without gauging its depth. Clarity in financial commitment ensures boundaries are respected and aspirations reachable.

Lack of planning often leads to shortfalls, like budgeting for a party only to find the bill much larger. Having defined saving and repayment goals aligns resources effectively, supporting long-range stability and satisfaction.