Most Americans believe they are middle class. It’s a deeply held self-image, practically a national identity. But there is a big difference between being solidly middle class and landing in the upper-middle-class tier, and in 2026, the gap between those two groups keeps widening. With inflation still pressuring budgets across the country and the cost of living varying wildly from state to state, figuring out exactly where your household stands has never been more complicated, or more important.

Honestly, the numbers might surprise you. The income thresholds have shifted, and for many families that felt comfortably middle class just a few years ago, the math no longer adds up the same way. Whether you think you qualify or you’re just curious how close you really are, let’s dive in.

1. What Does “Upper Middle Class” Actually Mean in 2026?

The term “upper middle class” sounds neat, but there is no single official definition. The American middle class and its subdivisions is not a strictly defined concept across disciplines, as economists and sociologists do not agree on defining the term. That can make self-identifying confusing and often misleading.

The American upper middle class is primarily defined by using income, occupation, and education, and it consists mostly of white-collar professionals with above-average personal incomes and a higher degree of autonomy in their work. Think lawyers, engineers, physicians, accountants. These are not just income earners but credential holders.

In academic models, the term “upper middle class” applies to highly educated, salaried professionals whose work is largely self-directed. Many have postgraduate degrees. Household incomes commonly exceed $100,000, equivalent to $164,849 in 2025. That inflation-adjusted figure tells you just how much the real threshold has shifted over time.

2. The Core Income Range: Where the Threshold Sits Right Now

A commonly cited range is from approximately $106,000 to $250,000 per year, as reported by Yahoo Finance. Other sources define the upper-middle class as starting around $104,000 and going up to $153,000 in 2026, as per CNBC. The spread between those figures is enormous, and that is the crux of the debate.

Based on these numbers, a household of higher-income earners between $117,000 and $150,000 would still put you among American upper-middle-class individuals in most cities around the country in 2026. However, because location is such a major factor, some sources even say the upper limit can be as high as $250,000.

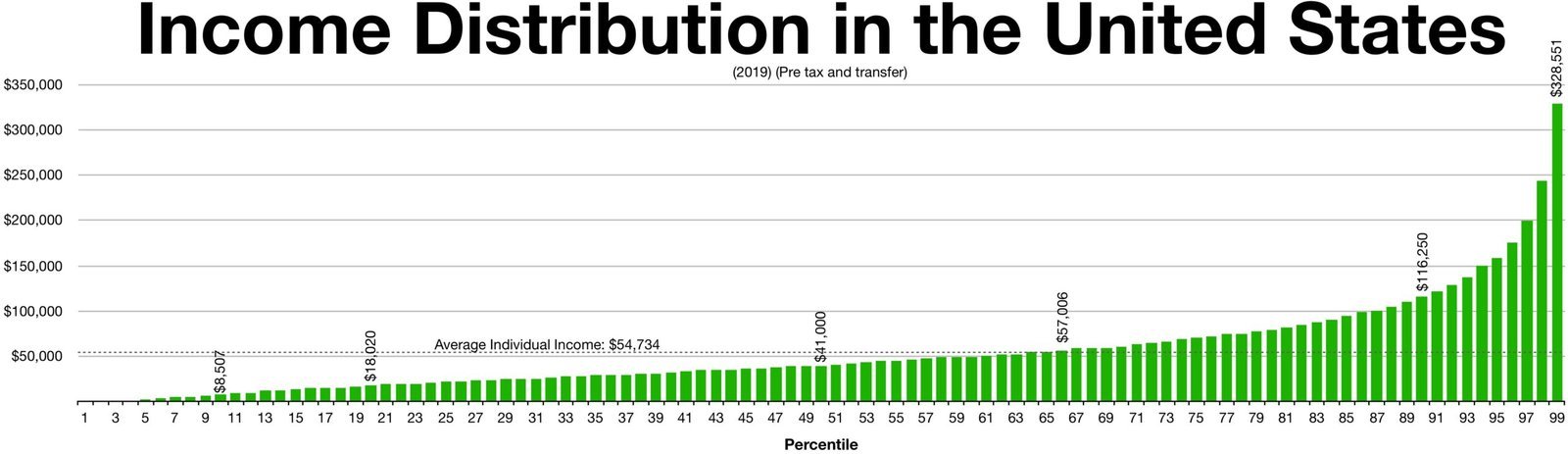

Based on the most recent U.S. Census Bureau data and the Pew Research Center, the median household income is listed at $74,580. So the upper-middle-class entry point begins at roughly one and a half times the national median. That puts it well within reach for dual-income professional households, but out of range for most single-income earners.

3. How Pew Research Defines the Income Tiers

Middle-income households, those with an income that is two-thirds to double the U.S. median household income, had incomes ranging from about $56,600 to $169,800 in 2022. In Pew Research Center’s analysis, “middle-income” Americans are adults whose annual household income is two-thirds to double the national median, after incomes have been adjusted for household size.

About half of U.S. adults, roughly 52 percent, lived in middle-income households in 2022, according to a Pew Research Center analysis. Roughly three-in-ten were in lower-income households and 19 percent were in upper-income households. So less than one in five Americans actually qualifies as upper income by that definition.

Based on the definition of the middle class, the income range for this group is anywhere from $56,600 to $169,800. That means that to be considered in the top 20% of the middle class, you would need to earn between about $117,000 and $150,000. That top slice of the middle class is essentially the gateway to the upper-middle-class designation.

4. Why Location Changes Everything

Here is the thing: your ZIP code may matter more than your paycheck. The same income that makes you feel wealthy in rural Ohio can leave you financially stretched in San Francisco. The difference is staggering, and it is reshaping how Americans understand their own economic standing.

According to GOBankingRates research, the median income varies tremendously by state due to the cost of living and employment possibilities. For example, if you live in Mississippi, a household income between $85,424 and $109,830 would put you in the upper-middle class. In Maryland, your household would have to bring in at least $158,126 to be considered in the upper-middle class.

Massachusetts has the highest threshold to break out of the middle class, with the upper bounds at $209,656 per year. New Jersey is close behind with an upper bounds of $208,588 on the middle class, followed by Maryland at $205,810, Hawaii at $201,490, and California at $200,298. Earning $200,000 in one of those states does not necessarily make you wealthy. It might still leave you firmly middle class.

5. The Role of Inflation in Shifting the Bar Upward

Inflation is quietly doing what most employers won’t: pushing the threshold for upper-middle-class status higher every year. In 2026, it is possible that the income range defining the upper-middle class could shift upward due to factors such as inflation. The expected annual inflation rate this year has risen to 2.6%. Moreover, the core inflation rate is expected to rise to 2.8%, according to the Commerce Department’s Personal Consumption Expenditures Price Index.

This ongoing price growth means households must earn progressively more just to maintain their existing standard of living. Daily expenses, including groceries, utilities, healthcare, and education, continue rising faster than traditional wage growth in many sectors.

Families that earned their way into upper-middle-class status in previous years may find themselves squeezed if their income growth lags behind inflation rates. This dynamic forces households to continuously reassess their financial position relative to evolving economic benchmarks. Standing still, in other words, is the same as falling behind.

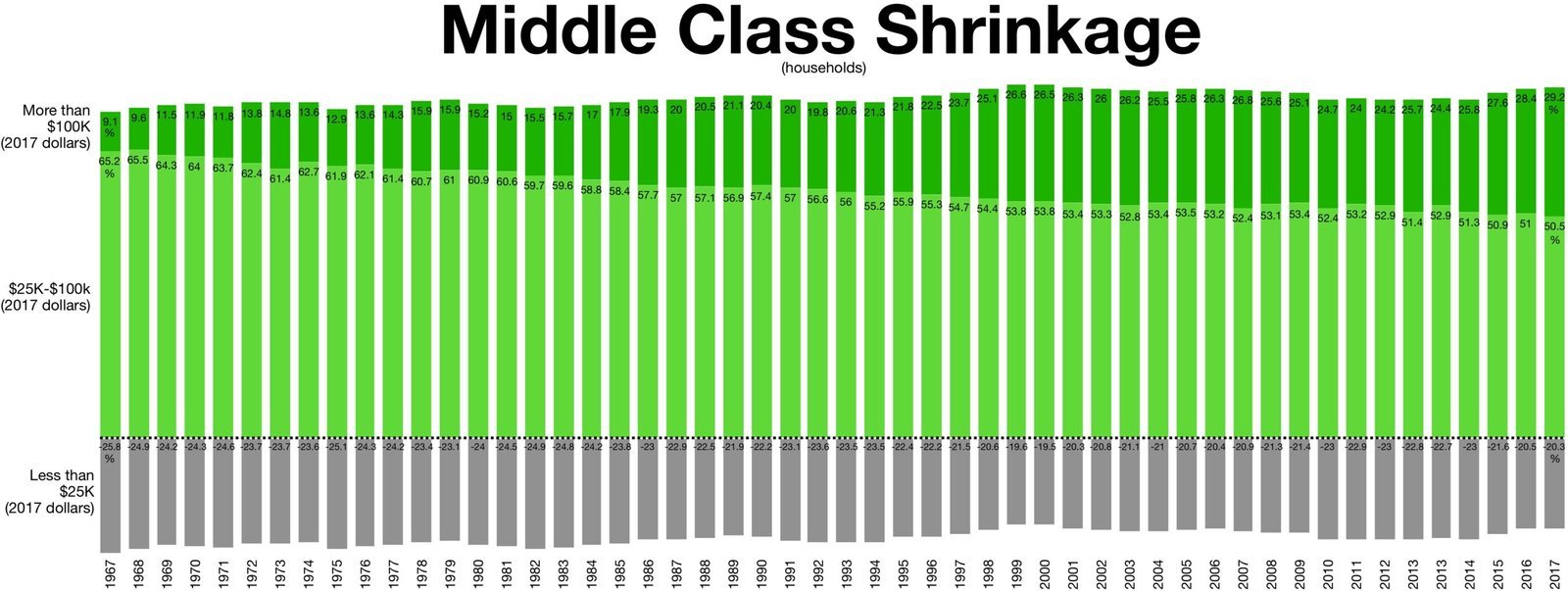

6. The Shrinking Middle Class: A Long-Term Trend

The middle class itself has been quietly hollowing out for decades, and the data confirms it is still happening. The share of Americans who are in the middle class is smaller than it used to be. In 1971, 61% of Americans lived in middle-class households. By 2023, the share had fallen to 51%, according to a new Pew Research Center analysis of government data.

From 1971 to 2023, the share of Americans who live in lower-income households increased from 27% to 30%, and the share in upper-income households increased from 11% to 19%. Notably, the increase in the share who are upper income was greater than the increase in the share who are lower income.

I think this pattern matters more than people realize. The middle class is not just shrinking. It is polarizing. Some people are moving up, which is encouraging, but the bottom is expanding too. Among Americans, 54 percent say they belong to the middle class, according to a 2024 survey from Gallup. Additionally, 31 percent identify as working class, 12 percent as lower class and just 2 percent identify as upper class. Self-perception and economic reality are clearly not aligned.

7. Education, Occupation, and What Really Gets You There

Income numbers are only part of the picture. The American upper middle class is primarily defined by using income, occupation, and education; it consists mostly of white-collar professionals with above-average personal incomes and a higher degree of autonomy in their work. The main occupational tasks of upper-middle-class individuals tend to center on conceptualizing, consulting, and instruction.

Education matters for moving into the middle class and beyond. Among Americans ages 25 and older in 2022, 52% of those with a bachelor’s degree or higher lived in middle-class households and another 35% lived in upper-income households. The degree remains a genuine financial accelerator, not just a credential on a wall.

More than a third, between 36% and 39%, of workers in computer, science and engineering, management, and business and finance occupations lived in upper-income households in 2022. These are the fields consistently placing people in that coveted upper-income bracket. Common professions within the upper middle class include lawyers, physicians, engineers, professors, and corporate executives. Pursuing higher education is a critical factor in attaining these prestigious positions and achieving upper-middle-class status.

8. Net Worth Matters Too, Not Just Annual Income

Here is something that often gets overlooked: income is what you earn, but wealth is what you keep. A household earning $150,000 a year that carries heavy debt, owns no assets, and saves nothing is not truly upper middle class in any meaningful financial sense. Net worth paints a fuller picture.

The upper middle class, also known as the mass affluent, is loosely defined as individuals with a net worth or investable assets between $500,000 and $2 million. Investable assets means money outside of your primary residence, which is considered “trapped.”

From a net-worth perspective, most experts agree that the threshold for upper class in the U.S. by 2026 will sit somewhere between $2 million and $5 million. So the upper-middle-class zone for net worth sits well below that, in the half-million to two-million range. A household earning $200,000 but saving very little, carrying large fixed expenses, and parking cash in low-interest accounts may not actually be building long-term security. Meanwhile, a household earning $140,000 that consistently saves, invests, and avoids lifestyle inflation can quietly build far more stability.

9. The Key Habits That Keep People in the Upper Middle Class

Getting into the upper-middle-class income bracket is one thing. Staying there is another challenge entirely. You are on track to leave the middle class when you have accumulated capital and are making that capital work for you. The key difference between someone who is truly wealthy and the middle class is that the wealthy make money when they are sleeping.

The foundation of wealth building within the American class structure lies in maximizing not only your paycheck but also increasing where you earn income. Relying on a single source of income is risky; to bring in more passive income, consider starting a side hustle. Multiple income streams are a common feature of upper-middle-class households.

Avoiding lifestyle inflation lets net worth compound while income-focused earners spend everything they make. Middle-class savers put money aside after paying bills. Wealthy people save before spending anything else. It sounds simple, almost boringly simple, but few people actually practice it consistently over the long term.

10. How to Check if You Hit the 2026 Upper-Middle-Class Threshold

So let’s be real: the simplest question is how do you know if you qualify? If you make between about $117,000 and $150,000, then you would probably be considered upper-middle class in most states at the turn of 2026. However, the actual amount of income you need depends on various factors, such as household size and the affordability of your residential location.

In the U.S., the upper middle class typically includes professionals and households with incomes well above the national median, but below the top 5%. With new IRS tax brackets and cost-of-living adjustments for 2026, understanding where your income fits can help you plan smarter for taxes, savings and long-term financial goals.

It is hard to say for sure that one number applies to everyone, because it simply does not. The Pew Research Center defines middle-income Americans as those whose annual household incomes are two-thirds to double the national median, adjusted for local cost of living and household size. Running your income through Pew’s interactive calculator at pewresearch.org remains one of the most reliable personal tests available today. The answer may be more surprising, or more humbling, than you expect. What would you have guessed before reading this?