Turning 60 is already a strange kind of checkpoint. You’re not old, but you’re not not old either. You start doing the math in your head: how many working years left, how much in the accounts, what does retirement actually cost? For me, those calculations got loud enough that I did something drastic. I committed to a full no-spend year – twelve months of stripping out every non-essential dollar and redirecting it as aggressively as I could toward financial security.

What followed was one of the most eye-opening, occasionally maddening, and surprisingly freeing experiences of my financial life. I didn’t expect the results to be this concrete. Let’s dive in.

1. The Starting Point Was More Uncomfortable Than I Expected

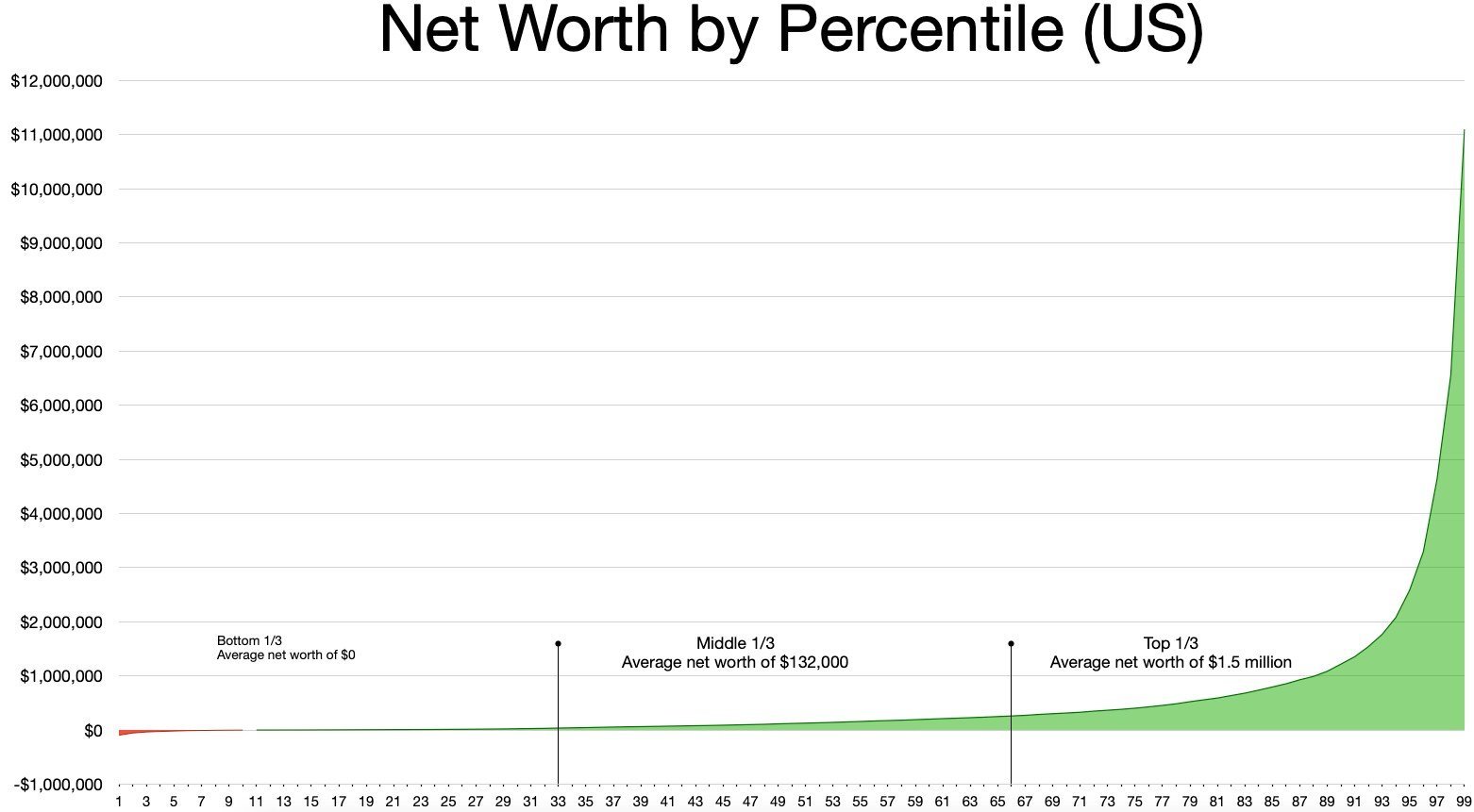

Before we even talk about what changed, let’s be real about where things stood at the start. The “magic number” Americans think they need to retire comfortably is $1.26 million, though that’s still a far cry from what most people have saved in their various retirement accounts. I knew I was behind. Knowing and accepting that are two different things.

The median retirement savings for those aged 55 to 64 sits at around $185,000 – nowhere near the million-dollar figure most people dream of. I wasn’t at the median. I wasn’t at the goal either. That gap was the entire reason I started this experiment.

By age 60, not even half of non-retirees with a retirement account or pension view their retirement savings plan as being on track. I sat with that statistic for a while. Then I opened a spreadsheet and got honest.

2. My Retirement Contributions Jumped Dramatically

The most immediate financial win from going no-spend was the amount I could redirect into tax-advantaged retirement accounts. This is where being 60 specifically matters, because the rules actually favor you. In 2026, workers can contribute up to $24,500 to a 401(k), or $32,500 if you’re 50 or older, and up to $35,750 if you’re between 60 and 63 years old – through so-called “super catch-up” contributions.

As of 2025, workers aged 60 to 63 can contribute an extra $11,250 to their 401(k) each year through this new increased catch-up provision. That’s not pocket change. That’s a serious wealth-building lever that most people in their 60s simply don’t use because their spending eats it up first.

I used it. Every dollar I freed from non-essential spending went straight into the accounts. Watching that number climb felt, honestly, a little addictive in the best possible way.

3. My Emergency Fund Finally Hit the Recommended Mark

Here’s something embarrassing: I was 60 years old and still didn’t have a proper emergency fund. Turns out, I wasn’t alone. In 2024, only 55 percent of adults said they had set aside money for three months of expenses in an emergency savings or “rainy day” fund – up slightly from 54 percent in 2023, but down from a high of 59 percent in 2021.

Thirty percent of adults indicated they could not cover three months of expenses by any means. That statistic is genuinely alarming for anyone approaching retirement age. An unexpected car repair or medical bill can derail everything when you’re on a fixed income runway.

By month four of the no-spend year, I had three months of expenses set aside. By month nine, it was six months. Unexpected expenses can strike at any time, and having an emergency fund can provide a critical safety net – experts recommend saving three to six months’ worth of expenses. I finally had it.

4. Subscription Creep Had Been Silently Draining Me for Years

I know it sounds crazy, but I genuinely had no idea how much money was leaving my accounts every month on autopilot. Streaming services, software subscriptions, membership renewals, digital storage plans, premium tiers for apps I barely opened – it was a slow leak that had been bleeding me for years.

Subscription creep continues to be a real issue for households, with streaming service spending alone growing from $26.50 to $29.80 per month – a notable increase that could reflect incremental price increases across platforms. When you multiply that across a dozen different services, it snowballs fast.

I cancelled everything I couldn’t justify within the first two weeks of the challenge. The annual savings surprised me. It’s the financial equivalent of finding money in a coat you haven’t worn in three years – except it just keeps showing up every single month.

5. Food Spending Was My Biggest Blind Spot

I thought I was a pretty reasonable spender when it came to food. I wasn’t eating at Michelin-starred restaurants or anything. Then I actually tracked it. The combination of dining out, food delivery, and impulse grocery buys was staggering.

Food delivery remains a dominant spending bucket in the discretionary category, with spending increasing to around $179 per month – a rise of roughly ten percent year over year. That’s nearly $2,200 a year just on delivered food. Added to restaurant spending, it becomes a very significant number very quickly.

Cooking at home became non-negotiable. Dedicating time to skip restaurants and takeout options can significantly reduce weekly food expenses – and sometimes even lead to discovering a genuine enjoyment of cooking. I wouldn’t say I found a passion for cooking exactly, but I did find an extra few thousand dollars a year. That felt better.

6. Debt Got Attacked in a Way It Never Had Before

Before the no-spend year, I was making minimum payments on a small remaining mortgage balance and a lingering credit card balance. It felt manageable, so I managed it – barely. The no-spend year changed that approach entirely.

Nothing can derail a retirement plan as quickly as high-interest debt – especially from credit cards. Aiming to retire debt-free if possible is a critical financial goal. That idea landed differently at 60 than it would have at 40. Retirement is no longer hypothetical. Carrying debt into it felt genuinely dangerous.

I threw every available freed-up dollar at debt first. Making large purchases and paying down debt before retirement and while still earning income is a strategy experts consistently recommend. I knocked out the credit card balance entirely by month six. The emotional relief alone was worth the entire experiment.

7. My Investment Portfolio Started to Actually Move

Here’s the thing about compounding: it rewards aggression. When I was putting modest amounts into investments, the growth was modest. When I started funneling the no-spend savings directly into a diversified portfolio, the effect was markedly different. It’s not magic. It’s just math finally working in your favor instead of against you.

Compounding describes how money builds on itself, creating even more money over time in an exponential manner – and the more time you allow for compounding to work its magic, the greater your money will grow. Even at 60, those years between now and 70 or 75 are enough for compounding to do real work.

A no-spend challenge is more effective when the money you save is earning a healthy return. High-yield savings accounts can deliver returns of over five percent while allowing quick access to your money. I used both – a high-yield account for liquidity and a brokerage account for longer-term growth.

8. My Social Security Strategy Changed Completely

One of the quieter but genuinely powerful effects of the no-spend year was what it did to my Social Security thinking. When I was spending freely, I felt pressure to claim as soon as possible – age 62, get the money, deal with the reduced amount. The financial cushion I built during the no-spend year changed that calculus entirely.

Waiting past full retirement age can increase your Social Security benefit significantly. If you claim at 62, you may get around 70 percent of your full benefit – but if you wait until 70, you could receive 124 percent. That difference, compounded over a retirement that could last two or three decades, is enormous.

Social Security provides an average monthly benefit of $1,976 as of January 2025 and is estimated to replace only about 40 percent of annual pre-retirement income. Knowing that gap exists makes the delay-until-70 strategy not just appealing but practically necessary for anyone who wants a comfortable retirement.

9. My Net Worth Grew – But the Mindset Shift Was the Real Asset

By the end of twelve months, my net worth had moved meaningfully. The combined effect of debt elimination, increased retirement contributions, stopped subscription leaks, reduced food spending, and redirected investment dollars created a compounding improvement across every financial metric. Net worth is simply what you own minus what you owe – your assets minus your liabilities. Mine improved on both sides of that equation simultaneously.

But let me be straight about something. The most valuable thing I gained wasn’t a dollar amount. No-spend challenges can work in the short term to save money for a financial goal, but they can also work in the long run, helping you figure out what’s actually important to you. I found out I valued almost none of what I had been spending money on reflexively.

When people slow down, get intentional, and build simple financial systems aligned with their values, confidence returns – even in uncertain times. That confidence, honestly, was something money couldn’t have bought directly. The no-spend year gave it to me as a side effect.

Conclusion

Doing a no-spend year at 60 isn’t for the faint of heart. It requires confronting habits, renegotiating what comfort actually means, and sitting with a kind of intentionality that our spending culture actively discourages. But the financial results are real, documented, and frankly hard to argue with.

Saving money was the most common resolution made for the second year in a row, edging out staple resolutions like eating healthier and exercising more – and regardless of whether people made a resolution or not, over half of Americans say they plan to save more money in 2026. Most people want this. Few go all the way.

If you’re sitting on the fence about a no-spend period – even just six months, not a full year – the most honest advice I can offer is this: the version of you on the other side of it will have a very different relationship with money. Not a poorer one. A freer one. What would your net worth look like if you truly stopped spending for a year? What do you think – would you dare to try it? Tell us in the comments.